Value-Added Tax at a Glance

Value-added tax (VAT) is a tax levied on the value created—or “value added”—by a business when selling goods or providing services. In South Korea, a 10% tax rate applies to most standard-tax transactions.

The key point that new business owners must understand first is the following:

For general taxpayers, the VAT payable is, in principle, the amount remaining after deducting input tax—which is deductible from output tax—from the output tax.

In other words, the system is structured such that a business does not pay the full amount of VAT collected from sales; instead, it reports and pays the remaining amount after deducting the VAT already paid on purchases made for business purposes.

Basic Definition of Value-Added Tax

Value-Added Tax is a tax levied on the supply of goods, the supply of services, and the import of certain goods. In practice, it is often referred to as “VAT” for short.

What Is Value Added?

Value added is the value newly created by a business operator during a transaction. From the perspective of a novice business owner, it can be understood roughly as follows.

| Category | Meaning |

|---|---|

| Sales Revenue | The amount received from selling goods or services, excluding VAT |

| Purchase Cost | The amount spent to produce or sell goods, excluding VAT |

| Value Added | The newly created value obtained by subtracting purchase costs and other expenses from sales revenue |

For example, if you purchased materials for 600,000 won, manufactured a product, and sold it for 1,000,000 won, the simplified value added would be 400,000 won. Applying the standard tax rate of 10% for general taxpayers, the VAT corresponding to this value added would be 40,000 won.

However, in actual tax filings, the tax is not simply calculated by multiplying the profit on the income statement by the tax rate; instead, output tax and input tax are calculated based on supporting documents such as tax invoices, credit card sales, and cash receipts.

Who Bears the VAT Burden and Who Pays It?

A key feature of VAT is that the person who actually bears the tax burden is different from the person who files and pays the tax.

| Role | Description |

|---|---|

| Taxpayer | The person who bears the economic burden of the tax. Generally, this is the end consumer. |

| Taxpayer | The person who bears the economic burden of the tax. Generally, this is the end consumer. |

When consumers purchase goods or services, they pay the VAT included in the price. Businesses collect that VAT on their behalf, hold it in trust, and then remit it to the government during the designated filing period.

Therefore, the VAT a business receives from customers is not net profit. Even if it is in the business’s account, it is essentially an amount that must be reported and paid later. To avoid cash flow shortages when VAT is due, it is helpful to set aside the estimated VAT in a separate account each time sales are generated.

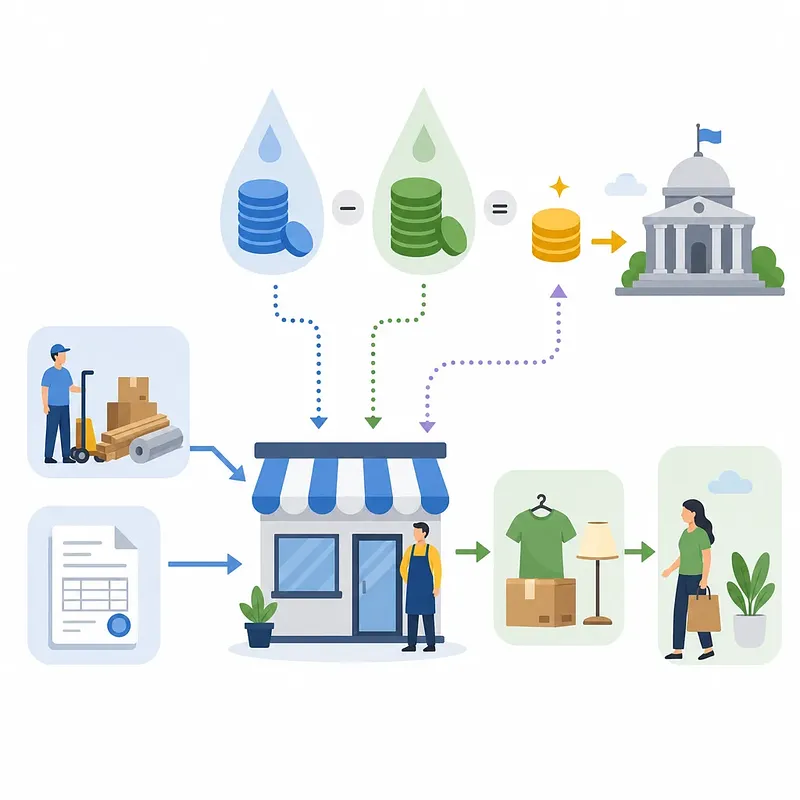

The Key to VAT Calculation: Output Tax and Input Tax

To understand value-added tax, you must distinguish between output tax and input tax.

| Term | Meaning | Example |

|---|---|---|

| Output Tax | VAT received when selling goods or services | Supply value of 1 million won × 10% = 100,000 won |

| Input Tax | VAT paid when purchasing goods or services | Supply value of 600,000 won × 10% = 60,000 won |

| Tax Payable | The amount remaining after deducting deductible input tax from output tax | 100,000 won – 60,000 won = 40,000 won |

The basic calculation formula for general taxpayers is as follows.

Value-Added Tax Payable = Output Tax – Deductible Input Tax

If the input tax exceeds the output tax, a general taxpayer may receive a refund for the difference, provided certain requirements are met. However, not all input tax is always deductible. Expenses not directly related to the business, input tax related to entertainment expenses, and certain passenger vehicle-related expenses may be subject to legal restrictions on deduction; therefore, you must verify supporting documentation and eligibility for deduction before actually filing your return.

Understanding the VAT Calculation Structure Through an Example

Let’s assume that Mr. A, who operates a bakery, conducted the following transactions.

| Item | Amount Excluding VAT | VAT | Amount Including VAT |

|---|---|---|---|

| Purchase of Ingredients | 600,000 won | 60,000 won | 660,000 won |

| Product Sales | 1,000,000 won | 100,000 won | 1,100,000 won |

President A paid 60,000 KRW in input tax when purchasing materials and collected 100,000 KRW in output tax from customers when selling bread.

Therefore, the simplified tax payable is as follows.

Output tax 100,000 KRW - Input tax 60,000 KRW = Tax payable 40,000 KRW

This is also equal to 10% of the value added (400,000 KRW), calculated excluding VAT.

Sales: 1,000,000 won - Purchases: 600,000 won = Value Added: 400,000 won

Value Added: 400,000 won × 10% = 40,000 won

This example illustrates why value-added tax is referred to as a “tax on value added.” In actual tax filings, the results may vary depending on factors such as industry, tax classification, tax-exempt or reduced-rate status, items subject to deduction limitations, and supporting documentation requirements such as tax invoices.

The Difference Between Supply Value and Supply Consideration

The terms “supply value” and “supply consideration” frequently appear when discussing VAT. Confusing these two terms can easily lead to misunderstandings regarding quotations, tax invoices, credit card sales settlements, and reported amounts.

| Term | Meaning | Calculation Example |

|---|---|---|

| Supply Value | The price of goods or services excluding VAT | 100,000 won |

| VAT | The tax amount applied to the supply value | 100,000 won × 10% = 10,000 won |

| Total Transaction Amount | The total transaction amount including VAT | 110,000 won |

In a standard-tax transaction where a 10% tax rate applies, the calculation is as follows:

Transaction Amount = Supply Value + VAT

VAT = Supply Value × 10%

Transaction Amount = Supply Value × 1.1

Supply Value = Supply Price ÷ 1.1

For example, if a consumer pays 110,000 won, this amount can be considered to consist of a supply value of 100,000 won and VAT of 10,000 won.

Differences Between General Taxpayers, Simplified Taxpayers, and Tax-Exempt Businesses

VAT is not applied in the same way to all businesses. The filing and payment structure may vary depending on a business’s tax classification and industry.

| Category | Key Features | VAT Filing and Payment Perspective |

|---|---|---|

| General Taxpayers | Businesses subject to the standard VAT taxation method | The basic structure involves deducting input tax credits from output tax. |

| Simplified Taxpayers | A tax classification applied to small-scale businesses that meet certain requirements | The calculation method differs from that of general taxpayers, as it reflects industry-specific value-added rates and other factors. |

| Exempt Businesses | Businesses that supply goods or services exempt from VAT | Instead of collecting VAT on transactions, the deduction of related input tax also differs from that of general taxpayers. |

| Businesses Subject to the Zero Rate | Businesses engaged in specific transactions subject to a 0% tax rate | Although output tax is zero, a refund of related input tax may be possible if certain requirements are met. |

New business owners should first verify the tax classification listed on their business registration certificate, determine whether the goods or services they supply are taxable or tax-exempt, and check whether they are required to issue electronic tax invoices.

Filing Deadlines and Practical Considerations

The deadlines for filing and paying VAT in Korea vary depending on the business type. Generally, individual general taxpayers often file final returns in January and July, while corporate taxpayers file more frequently, including both estimated and final returns. The filing methods and cycles for simplified taxpayers differ from those for general taxpayers.

Since the exact filing deadlines may vary depending on the applicable tax period, business type, whether the business is temporarily suspended or closed, and tax law amendments, you must check the National Tax Service guidelines and the HomeTax filing screen.

Points for Beginner Business Owners to Pay Particular Attention To

- Do not treat the VAT included in sales as gross profit.

- Keep all eligible supporting documents—such as tax invoices, receipts, credit card slips, and cash receipts—without exception.

- VAT on expenses unrelated to your business may not be deductible.

- If you have both tax-exempt and taxable sales, calculating input tax credits can become complicated.

- Omitting sales or fabricating purchases can increase the risk of surcharges and tax audits.

Simple Methods for VAT Cash Flow Management

Since VAT is paid in a lump sum during the filing period, even with steady sales, poor cash flow management can lead to a significant financial burden at the time of payment.

In practice, the following methods are helpful:

- Transfer the amount equivalent to VAT from your sales receipts to a separate account.

- At the end of each month, roughly calculate the output and input tax amounts to estimate the expected payment.

- Regularly verify whether you have received tax invoices and check your credit card and cash receipt documentation.

- Organize your records on a quarterly or monthly basis, rather than waiting until just before filing.

- If your sales volume increases or your transaction structure becomes complex, consult with a tax agent.

Key Points

Although VAT is a tax levied on the value added by a business, the actual economic burden is borne by the end consumer. Businesses collect VAT from consumers, hold it in trust, and then report and pay it.

For general taxpayers, the most important formula is as follows:

VAT payable = Tax on sales - Deductible input tax

When reviewing transaction amounts, you must distinguish between the supply value and the supply consideration.

Supply Value = Price excluding VAT

Consideration for Supply = Price including VAT

For novice business owners, it is most important to view VAT not as a “tax to be paid later,” but as an “amount that was never your money to begin with.”